Will Supply Chain Problems Bring Down Stocks?

Too Much Demand is the Key U.S. Economic Issue

In a typical recession, households lose employment, disposable income levels fall or plateau, consumer spending declines, credit markets tighten up, and banks issue fewer loans. The result is that demand falls across the economy, with less money going towards goods and services.

We see the opposite happening today.

In the U.S., the unemployment rate is hovering around 5%, disposable incomes are higher, and households are sitting on roughly $1.6 trillion in savings. That’s because the pandemic was not a typical recession, nor did it trigger a credit event, a financial crisis, or damage to household balance sheets. In fact, U.S. households are largely better off today than they have been at any point in history.(1)

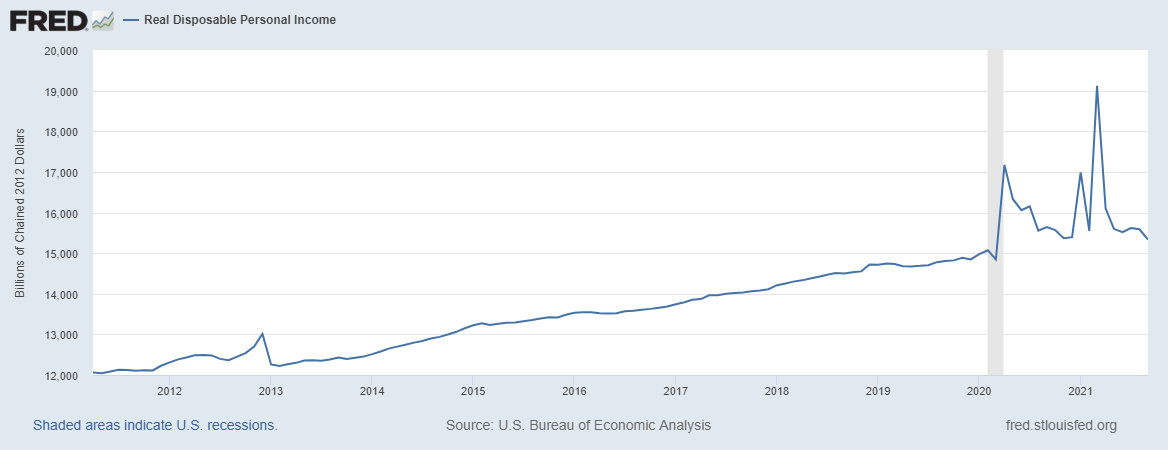

Allow me to offer a quick analysis in charts. First, real disposable incomes (adjusted for inflation) are close to $16 trillion in the U.S., which has been driven higher by direct transfers from the federal government through stimulus programs but also via higher wages. There have been many reports of labor shortages in the U.S., but it is also true that many workers are finding they can easily switch jobs for higher wages. Desperate to fill positions, many employers have been raising wages as a result. According to the Labor Department, private-sector hourly wages were up 4.6% year-over-year in September.

Real Disposable Personal Income

Source: Federal Reserve Bank of St. Louis (2)

Source: Federal Reserve Bank of St. Louis (2)

These higher wages, combined with accumulated savings, a rising stock market, and the strongest housing market in over a decade have also given way to record household net worth in the U.S.:

Household Net Worth

Source: Federal Reserve Bank of St. Louis (3)

Source: Federal Reserve Bank of St. Louis (3)

Put these fundamentals all together, and you have a situation where the U.S. economy has what I would call a good problem: too much demand.

In my view, the biggest driver behind snarled supply chains and shortages of goods and services is not policy failures or systemic economic issues – it’s that the U.S. and global economy simply do not have the current capacity to meet this wall of demand. And that’s a good problem.

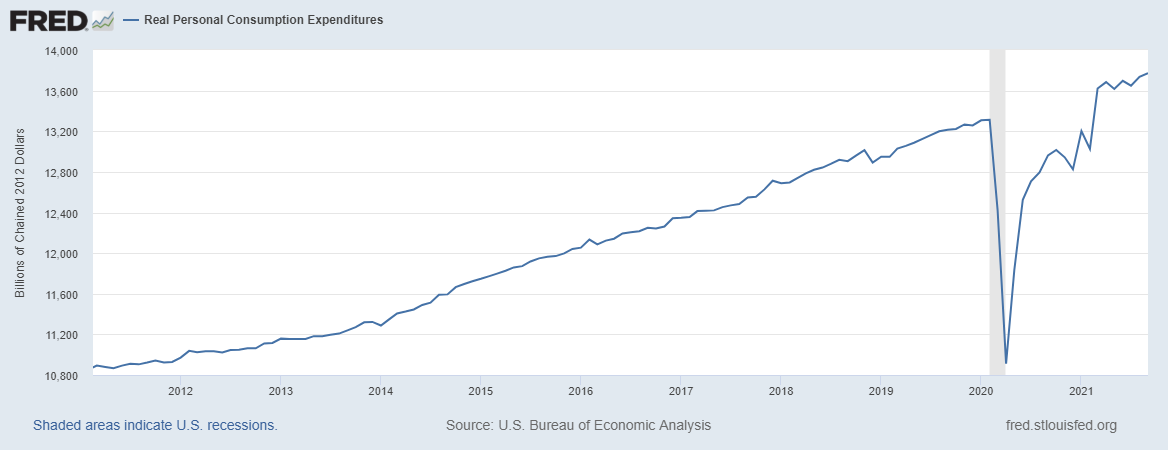

Consumers are showing few signs of slowing down. According to the Commerce Department, inflation-adjusted retail spending has soared by 14% in the last two years, which is a bigger increase than the previous seven years combined. Retail sales rose 13.9% in September from a year earlier, and sales at retail stores, restaurants, and online sellers were up nearly 1% month-over-month. The momentum favors even more spending – in the first week of October, retail spending was up 8.8% compared to the average week in September.

U.S. Consumption Expenditures: Still at or Near All-Time Highs

Source: Federal Reserve Bank of St. Louis (4)

Source: Federal Reserve Bank of St. Louis (4)

To be fair, the ‘good problem’ of too much demand does not automatically have a happy ending. Persistent supply chain issues could continue to drive prices higher, which could discourage spending and result in declining consumer sentiment for future quarters. The economic calculus is in determining which might happen first: inflation drives consumers away, or corporations and the global economy expand capacity and ultimately catch up to demand. In my view, it’s the latter.

Bottom Line for Investors

The U.S. consumer is in a historically strong position, and I would argue the current cash glut in the U.S. economy is a key determinant in supply chain issues. Simply stated, there is so much demand that supply can’t keep up.

In my view, this is a good problem. U.S. consumers’ financial position is not likely to change significantly in the next six months or so – if anything, it could get even better as more enter the workforce and wages continue to move higher. Meanwhile, corporations and supply chains are likely to find ways to catch up relatively soon, which should give way to sustained levels of higher spending. A good problem, with a good outcome. As always, we welcome the opportunity to discuss how this affects your personal finances.

Kevin M. Collier President Collier Wealth Management, Inc. 323 West Main Street Hendersonville, TN 37075 Phone: 615-826-5203Important Information

(1) Wall Street Journal. October 24, 2021. https://www.wsj.com/articles/economy-week-ahead-central-banks-gdp-consumer-spending-11635102000

(2) Fred Economic Data. October 1, 2021. https://fred.stlouisfed.org/series/DSPIC96

(3) Fred Economic Data. September 23, 2021. https://fred.stlouisfed.org/series/BOGZ1FL192090005Q

(4) Fred Economic Data. October 1, 2021. https://fred.stlouisfed.org/series/DSPIC96

LPL Tracking No. 1-05209178